STRATEGY —

The Roll-Up Math Just Broke

The cheapest way to take a category is no longer to buy it.

TL;DR: For thirty years the move in a fragmented market was to buy the software-defended incumbent cheap and sell the consolidated platform high. In 2026 that broke. Public software multiples compressed about forty percent, debt got expensive, and when a category's moat is just aging software, building the replacement now costs a fraction of buying the leader. But the trade only flips for narrow moats. Deep data, workflow, and compliance lock-in still hold, so the real question before you wire a dollar is whether the moat is the software, or the thing the software is sitting on.

The Trade That Ran for Thirty Years

For thirty years the smartest play in a fragmented industry was simple. Find the under-systematized businesses. Buy them at six to eight times EBITDA (earnings before interest, taxes, depreciation, and amortization). Centralize the back office, bolt on some software, sell the combined platform at twelve to fifteen times. Cheap money in, expensive multiple out. I have run versions of that deal more times than I can count, and I still teach it.

This year, in a growing list of categories, it broke. Not in theory. On the smart money's own books.

The numbers are not subtle. Public software multiples have compressed by something close to forty percent, the median falling from around five and a half times revenue to roughly three and a half as buyers price in the threat of AI disruption. The exact trade I just described, buy the software-defended incumbent and ride the multiple up, is the one the most sophisticated buyers in the world are now quietly backing away from. When capital that committed to a strategy for thirty years moves that fast, it is worth understanding what it just saw.

What it saw was that the old engine had stopped turning. There is nearly four trillion dollars of private-equity dry powder that still has to go somewhere, but money now costs eight to nine percent, so the leverage that used to do the heavy lifting has thinned to about a third of the deal.

You can no longer buy a multiple and wait for it to expand. You have to manufacture the earnings growth yourself, under the hood, or the math never closes. And the assets that used to make that easy, lower-middle-market software businesses, now trade around four and a half times revenue, with anything short of real retention or a credible AI answer dragged down to three.

When the Moat Is Just Software

Here is the mechanism, and it is sharper than "AI is eating software."

In most fragmented industries, the thing actually holding the customers in place is software. Aging, expensive, deeply embedded software the whole category complains about and almost nobody leaves. When you roll those businesses up, that software is half of what you are really paying for. The switching cost is the moat. The moat is why the multiple holds. Take the software away and you are buying a pile of small, ordinary businesses at a small, ordinary multiple.

So watch what happens when the software stops being hard to replace.

I'm Watching One Happen Right Now

I am watching one of these play out right now. A trades vertical. The incumbent platform is about thirty years old. Desktop heritage, endlessly customizable, no published pricing, you call for a quote. No real mobile app. The shops that run it also pay for a separate field app and a separate accounting system. Three logins, nothing connected, four to six hundred dollars a month for a five-person shop, and a daily tax of double entry and exported spreadsheets that everyone has simply accepted as the cost of doing business.

A small team is rebuilding the whole thing as one app. Two hundred dollars a month, flat. Mobile first. It does the daily work in a third of the clicks. And it does one thing none of the incumbents will ever do: it uses AI to generate the regulatory paperwork, grounded in the actual local code. That is not a feature the legacy guys forgot to ship. It is a feature they are structurally not built to ship, because their architecture was set before any of this was possible.

Run the two numbers side by side. Cost to acquire that incumbent: call it fifteen million, leveraged and board-approved. Cost to build the thing that makes it optional: closer to five hundred thousand.

Same customers. Same category. A fraction of the capital, and none of the baggage. When you build the replacement instead of buying the leader, you inherit no legacy codebase, no eighteen-month migration that runs eighteen months over, no earnout you overpaid to make the seller comfortable, and no customers who only stayed because leaving was a nightmare. You start clean, and you start cheap.

The sharpest operators do not even pocket the difference. They spend it. You take the fourteen and a half million you did not hand the seller and you point it straight at distribution, paying to buy customers out of the incumbent's multi-year contracts, funding the kind of growth loops the legacy player's margins could never survive. The capital that used to buy the company now buys the market instead.

Which Incumbents Actually Melt

That asymmetry is why the challenger field exploded. In category after category the contest went from three incumbents to three hundred startups, and the three hundred carry none of the architectural debt the three are dragging. There is a deeper reason they can move so fast. The work itself is detaching from the screen.

AI agents increasingly operate above the interface, talking to the underlying systems directly, which quietly dissolves the one moat the old guard counted on more than any other: that everyone in the industry was trained on their software and nobody wanted to relearn another. When the agent does the clicking, "everyone already knows our screens" stops being worth anything.

But here is the part most operators get wrong, and it is the difference between a smart move and a hot take. This does not mean all software is replaceable. It means the narrow kind is.

You could rebuild the first version of a category-defining platform ten times faster today.

You could not rebuild what it became: years of accumulated, proprietary data, deep integration into the customer's daily workflow, real regulatory and compliance lock-in.

AI's lift is uneven. It helps the hungry challenger far more than the entrenched leader, so it melts the thin moats, a clean interface, a switching cost, a single clever feature, and leaves the deep ones standing.

So before you write the check, look hard at which kind of incumbent you are actually buying. The vulnerable one has tells: an aging interface, a moat that is mostly switching cost and inertia, no proprietary data that compounds, nothing a generic tool could not eventually copy.

The durable one owns data a new entrant cannot get, sits in the center of a workflow that would be painful to unwind, and carries compliance a clone cannot fake. The question is no longer "does this business have software." It is "is the moat the software, or the data and the workflow the software is sitting on?"

That single question flips the operator's whole approach. Walk into a fragmented market and the reflex is to ask "what should I buy?" In a category whose moat is just software, that is the wrong question. The better one is "what here could I make worthless?" The answer is usually the aging incumbent everyone assumes is too entrenched to touch, the one whose customers complain every year and renew every year anyway.

The Trojan-Horse Version

There is a hybrid for operators who want the distribution without the wait. Buy the tired incumbent, but buy it cheap, at distressed prices, and buy it for one thing only: its customer base and its channel. The day the deal closes you do not try to save the old software.

You rip the stack out, drop your lightweight version in behind the same logins, and the margins that were trapped under thirty years of technical debt snap toward ninety percent almost overnight. You did not pay the platform multiple. You paid for the distribution and built the moat yourself.

My Perspective

None of this is an anti-acquisition sermon from a man who loves acquisitions. Most categories are not software categories, and the roll-up is far from dead. I am telling you to add one question before you wire a dollar. Is the moat I am paying for real, or is it just software somebody with a laptop and a year could rebuild for two hundred a month?

It helps to remember this is an old pattern, not a new panic. When the FORTRAN language made programming easy in the 1950s, the programmers of the day were certain the craft was finished, that making it simple would make them worthless.

Over the next two decades the number of programmers in the United States grew thirty to fifty times.

Commoditizing a layer does not end the game. It changes who wins it, and it almost always rewards the people who saw the shift early and moved while everyone else was still defending the old position. The operators who take these categories over the next decade will not be the ones who bought the most. They will be the ones who looked at the leader everyone was afraid to challenge and asked the cheaper question first.

— Roland

P.S. If building the replacement is this cheap, the uncomfortable version of the question points the other way. The business you are about to buy, or the one you are about to sell, how much of its value is just software somebody could rebuild for two hundred a month? That is Friday's letter. I call it the melting ice cube.

Want more than just the weekly deep dives?

On Instagram we share quick tips, behind-the-scenes looks, and first access to what’s coming next.

Follow @RolandFrasier on Instagram and join the community.

Thinking About Exiting Your Business?

What Would Buyers See If They Evaluated Your Business Today?

Your Exit-Ready Score reveals the hidden risks that suppress valuation, built on the same indicators private equity uses to screen deals in under 5 minutes.

Find out your score….

Whats Going On Recently

Keep More Of Your Money: PRIME can show you how to protect yourself, grow assets, build business funding, and how to take advantage of 250+ unique tax deductions.

Zero Down Book | Free Copy

This Book Reveals Little-Known Wall Street Insider Strategy To Quickly Acquire Profitable Businesses Worldwide, Without Using Your Own Money or Credit...

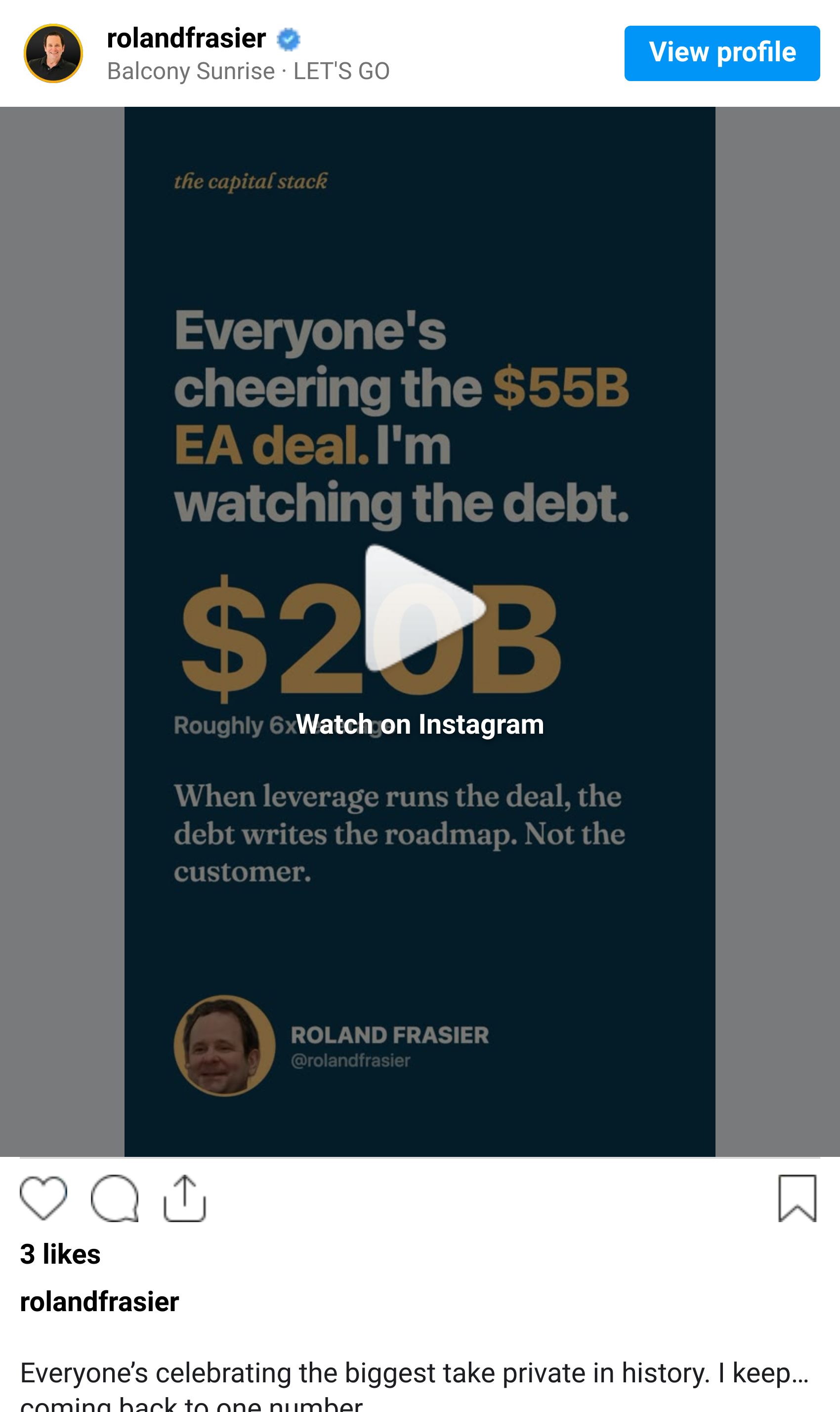

Roland’s Riff

Everyone is talking about the purchase price.

I’m looking at the debt.When a deal gets large enough, the question stops being “What was it worth?” and starts becoming “Who does the business answer to now?”

Most people see financing as a detail. In reality, capital structure shapes decisions, incentives, and priorities long after the headlines fade.

The numbers on the term sheet don’t just fund the future. They influence it.

Want to see how capital structure quietly becomes company strategy?

Watch the video below.